WHAT IS CARBON TRADING?

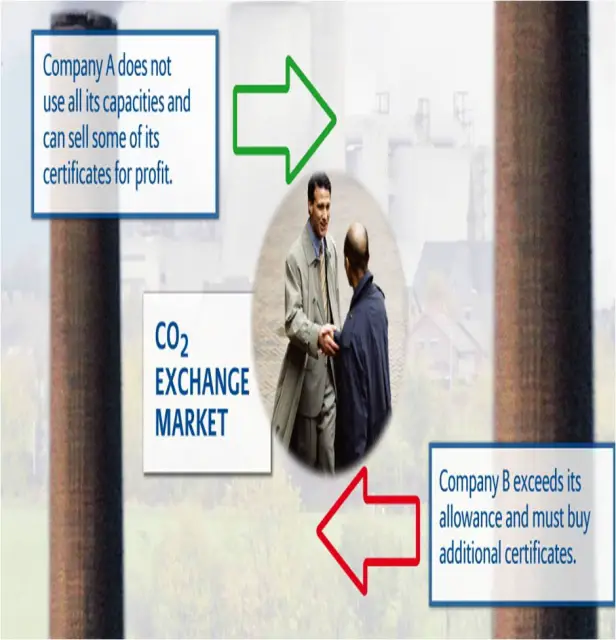

Carbon trading is a market-based scheme for environmental improvement that allows parties to buy and sell permits for emissions or credits for reductions in emissions of certain pollutants.

KYOTO PROTOCOL 1997

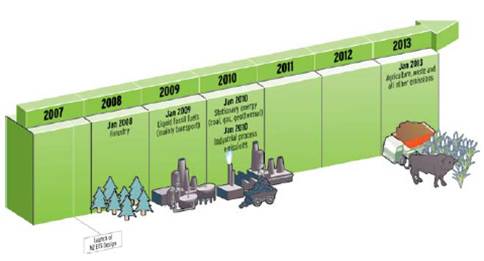

By Kyoto Protocol of 1997 by which all countries are required to reduce their greenhouse gas emissions by 5% –from 1990 levels– in the next ten years, i.e. 2012—or pay a price to those that do.

By Kyoto Protocol of 1997 by which all countries are required to reduce their greenhouse gas emissions by 5% –from 1990 levels– in the next ten years, i.e. 2012—or pay a price to those that do.- The Kyoto Protocol is a 1997 international treaty which came into force in 2005, which binds developed nations to a cap and trade system for the six major greenhouse gasses.

- Emission quotas were agreed by each participating country, with the intention of reducing their overall emissions to 1990 levels by the end of 2012. Under the treaty, for the 5-year compliance period from 2008 until 2012, nations that emit less than their quota will be able to sell emissions credits to nations that exceed their quota.

- It is also possible for developed countries within the trading scheme to sponsor carbon projects that provide a reduction in greenhouse gas emissions in other countries, as a way of generating trade able carbon credits.

Greenhouse gases (GHGs) are trace gases that control energy flows in the Earth’s atmosphere by absorbing infra-red radiation. Some GHGs occur naturally in the atmosphere, while others result from human activities. There are six GHGs covered under the Kyoto Protocol – carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), hydro fluorocarbons (HFCs), per fluorocarbons (PFCs) and sulphur hexafluoride (SF6). CO2 is the most important GHG released by human activities

HOW DOES IT WORK?

The idea was to make developed countries pay for their emissions while at the same time monetarily rewarding countries with good behavior in this regard. NGOs or non-profit organizations for long have been screaming for everybody’s attention towards this huge problem, but no one seems to care enough, not until there is a financial incentive attached to it. That’s what the governments of various countries have been trying to come up with, a trading mechanism where companies gain a monetary benefit out of polluting the air less.

They have various ways to generate these units:

- Invest in CDM/JI Projects.

- Buy these credits from the market0

- Energy intensive sectors such as the built environment have an ongoing commitment to recognise and reduce industry related emissions and their contribution to the global climate change.

- Carbon emissions trading is an essential policy response to climate change. An emissions trading scheme is an effective way to enable energy intensive industries to bring to account the costs of greenhouse gas emissions and for those costs to become part of the decision making processes of emitters.

- Buildings account for 8% of greenhouse gas emissions, or 20% if upstream emissions associated with electricity and heat are included. Emissions resulting from buildings include those associated with their construction, operation, maintenance and demolition of buildings.

- Embodied energy is an additional consideration as a proportion of whole-of-life energy consumption. There is considerable scope for emissions reduction or abatement resulting from energy.

CONSTRUCTIVE MEASURES

There are some measures that should be integrated by the property sector into the built environment. These include:

• Building fabric improvements

• Lighting systems (& greater use of natural light)

• Heating and cooling systems and control improvements

• Energy efficient motors

• Energy efficiency equipment (copiers, computers, appliances etc.)

• Passive design

• Onsite generation

Energy efficiency is, and will remain, a central element of a cost-effective greenhouse abatement strategy, delivering about 40 per cent of expected energy abatement in 2010. However, the market drivers that already exist for energy efficiency building design and operation can be further developed by inclusion of the built environment in the development of a carbon emissions trading scheme.

ETHICS

Lot of people argue that buying carbon units from the market does not give rights to pollute the environment. Meaning, you just cannot buy the rights to pollute the air. Well, first of all to believe that every human being on this earth will spend money just to keep the air clean is not true. Companies wont be involved until there is a financial benefit for doing so.

PROS OF THE SYSTEM

- The reduction in overall cost of meeting emission reduction targets,

- The progressively improved definition of a “price” for carbon, particularly as the market becomes more liquid and active, and assuming that all carbon certificate products are fungible, meaning that they are equivalent ways of addressing emission reduction;

- The opportunity to generate income from activities that previously attracted no additional revenue, such as investment in emission reduction, renewable energy generation, greenhouse friendly fuels and carbon sequestration;

- The ability to use revenue from carbon sequestration to help fund additional planting of trees and other vegetation, for benefits such as salinity amelioration, biodiversity enhancement, conversion to greenhouse gas friendly fuels and energy, and employment and wealth creation in rural areas.

- Permit prices may be unstable and therefore unpredictable

- Cap and trade systems are seen to generate more corruption than a tax system

- The administration and legal costs of cap and trade systems are higher than with a tax

- A cap and trade system is seen to be impractical at level of individual household emissions

- Its not really an attempt to reduce co2 ,its more of an superficial system of maintaining certain carbon dioxide level.

- Jindal Steel on Oct 19, said that the Corex furnace technology that it employs would prevent 15 million tonnes of carbon from being discharged into the atmosphere in the coming decade. At a sale price of $15/tonne that is a total of $225 million.

- Jindal says companies from the Netherlands, Canada, the US and Japan have begun talking to it.

- On Oct 22, the New Indian Express carried a story that said the World Bank had just handed over $10 million to India’s Infrastructure Development Finance Company to fund ‘clean’ projects that would generate saleable carbon credits.

- It’s true that the sudden boom in the carbon market has greatly helped Indian industries to cash in on the carbon trading business. India certainly being the preferred location for carbon credit buyers or project investors because of its strategic position in the world today.

- Unfortunately, there are very few consultants who understand the true potential of this market or in other words understand this market in totality. Most of the companies working in this area are just acting as middle men as small industry owners are not aware of this new market at all. Ironically, most of the industry owners who are interested in implementing a CDM Project have not heard of \”UNFCCC\” at all.

- Dr. Srinivasa had imagined a role for rural India in this emerging market. He said that power generated by naturally grown fuels would yield carbon credits and revenue from their sale should be factored into, when evaluating a bio-diesel future. Will we do it before the carbon market closes? If we could, would not bio-diesel power be unbeatable economics?

- India can tap the $52-billion global market for carbon trading by encouraging production and use of biofuels and plantation of trees having oil-bearing seeds and materials, like Jatropha and Pongamia species. Other plantations having oil-bearing seeds or materials are Sal, Mahua, Kokum, Pilu, Phulwara, Dhupa, Neem, Mango, Kusum, Karanja, Ratanjyot, Jatropa, Tumba, Jojoba, Simarouba

- Biofuels, apart from enhancing energy security, ensuring employment and development and mitigation environmental pollution, can be instrumental in carbon trading if certain criteria of the clean development mechanism (CMD) of the Kyoto Protocol of the United Nations Framework Convention on Climate Change (UNFCCC) are fulfiled, said experts

- Each tonn of bio-diesel produced or consumed leads to a reduction of GHGs by about three times ie avoids 3 tonn of CO2e.

- These reductions in GHG emissions can be accumulated and traded as carbon credits. The CMD facilitates selling of these reductions in terms of certified emission reductions (CERs), a unit of which equals to one tonn of CO2.

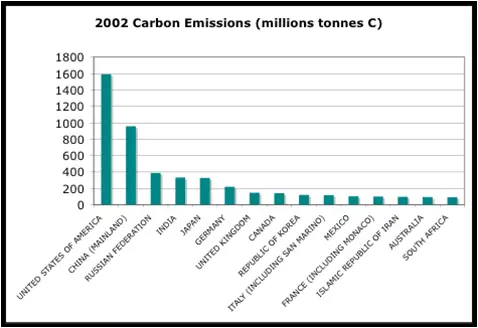

- Growing at a rate of 4% per year, India, the sixth largest producer of greenhouse gases (GHGs), contributing almost 3% of the world’s total emissions (including CH4 from waste generated by cattle) is seen as one of the most attractive destinations for CMD linked investments. Estimates put the cumulative foreign direct investment (FDI) on account of such projects at about $2 billion, growing at the rate of $200 per year.

CARBON TRADING AND INDIAN ECONOMICS

- INR 15,000 crore will be the Carbon credits sale proceeds by 2012 for India.

- The number of projects approved by national authority are biomass (197), energy efficiency (166) and renewable energy (151) . The list of Potential carbon credit volume contribution by type of projects is lead by energy efficiency (11.33 crore), with industrial process (0.97 crore) and biomass (0.61 crore) following.

- Region/State wise ranking of approved projects are 1) UP: 69 2) AP: 68 and 3) Maharashtra:68. China is leading with average annual reductions of 65,036,178 with 90 projects. India has 250 projects (35.06%) approved with average annual reductions of 22,998,713 .

- For Indian enterprises, the benefits have so far largely been availed of by small and medium enterprises (SMEs). Public Sector Units (PSUs) have mostly remained away, in large part due to lack of knowledge. For India to cash in on the vast potential of the carbon market, a government strategy needs to be devised to derive the maximum benefits from it and address current market failures.

- Private sector has a significant role to play as well. Many of the Indian projects are currently driven by SMEs and stand disadvantaged because each project generates a small quantity of carbon credits. In contrast, a buyer wishing to purchase a large volume of carbon credits can often buy the required amount from a single project in China. In India, the same quantity of carbon credits would have to be purchased from ten or more projects. Hence, the private sector needs to build its expertise to club small projects together in order to improve their market access.

- In the end, the growth of the carbon market will largely depend on the realization that the market can assist India in achieving low carbon growth, and the consequent development of a strategy to cash in on the opportunities this offers.

FACTS AND FIGURES

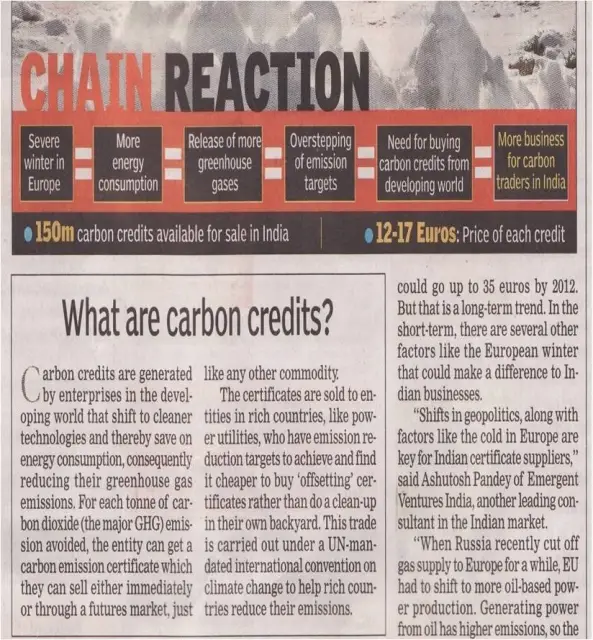

- The growing pressure on countries to address climate change has given rise to a multi-million dollar international market for buying and selling emissions of greenhouse gases. Under the Kyoto Protocol which came into force in February 2005, industrialized countries agreed to collectively reduce emissions of greenhouse gases by 5 percent by 2012 compared to 1990 levels

- In light of increased evidences of climate change effects and their mitigation methodologies, several carbon market and investment mechanisms are slowly evolving. Though the carbon market dynamics are not transparent, the scenario indicates a huge potential in future.

- Till January 2004, the total volume traded in project based transactions is 78 million tonne of carbon dioxide emissions (CO2e). The buyer side included Japan with 41 per cent, The Netherlands and CFB with 23% each. According to estimates, if the CMD captures at least 35% of the global market, the estimated value to the concerned countries would be $18 billion.

- The majority of projects that have sold carbon credits so far include renewable energy (such as wind power, biomass cogeneration and hydropower); energy efficiency measures in several sectors ( such as cement, petro-chemicals and power generation); as well as the reduction of industrial gases that contribute to climate change.

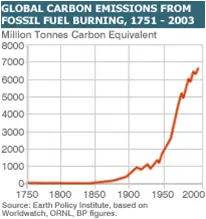

- The carbon market is already the fastest growing market in the world. Between 2003 and 2004, the volume of carbon credits sold by developing countries doubled, and then tripled between 2004 and 2005. In 2006 alone, carbon transactions worth $30 billion were conducted globally, transferring some $5 billion from the countries of the global north to the global south.

- the total number of carbon contracts signed in the world so far, India has the second largest portfolio with a market share of 12 percent, behind China which had a market share of 61percent.

- The Kyoto Protocol expires in 2012, and international talks have already begun to decide the shape of a new treaty that will succeed it. After 2012, the carbon market is expected to expand exponentially. Some say that it could grow to $100 billion annually, becoming a significant source of foreign capital flows from the developed to the developing world, on par with levels of Official Development Assistance.

The banking sector is already a key player in the shift to a low carbon economy… Federal regulation of carbon is now a realistic prospect – and already influencing corporate mergers and acquisitions

Leading companies have recognised the need for change

Leading companies have recognised the need for change and are:

- Cutting operational emissions on a voluntary basis;

- Backing long-term regulatory action to internalise a price for carbon;

- ‘Climate proofing’ existing goods and services; and

- Sizing market opportunities.

The carbon trading market, for example, is projected to be worth US$ 2 trillion a year by 2012, with opportunities to finance US$1.9 trillion in clean energy technologies by 2020

Investing in low carbon business

Barclays has provided the long-term finance for more than 2,600MW of renewable generating capacity, and to date has traded 300 million tonnes of carbon. Standard Chartered Bank invested US $800m in 2006 in renewable energy projects.

Committing to reduce carbon within investments

The World Bank has recently made a commitment to develop a greenhouse gas (GHG) assessment methodology to track the carbon footprint of its core development activities in the energy (including oil and gas) and transport sectors10. The Bank of America has committed to making a 7% reduction in indirect emissions within their energy & utility portfolio.

Dear Abhishek Jain, Apoorva

Dear Abhishek Jain, Apoorva Bajpai, Akshay Kulkarni, Rituparna Simlai, Swati Goel:

I have gone through your interesting and enriched article. I am a PhD student of University of Calcutta. My theses is ” GLOBAL SITUATION IN CARBON TRADING : INDIAN PROSPECT”. Would you please send me further materials to prepare my theses. Feel free to advise. Awaiting reply.

Best Regards,

Dibakar Pal

Dept. of Business Management

University of Calcutta